Bruno Pellegrino introduces a novel model developed with Enrico Spolaore and Romain Wacziarg that explains the lack of international investment in some countries despite their promise of higher returns. The study finds that removing certain barriers to international capital flows could boost global GDP by 7% and significantly reduce cross-country inequality.

Why does investment flow from certain countries to other countries? This seemingly simple question has long puzzled economists. International investment data, in fact, display several patterns that we would not expect if international investors were fully rational and cross-border investment was unimpeded.

Understanding these investment patterns is crucial, as they have profound implications for global economic growth and inequality between nations. Nobel laureate Robert Lucas famously observed in 1990 that, contrary to theory, capital flows only modestly from rich to poor countries, despite being much more productive in the latter group. This phenomenon is known as the “Lucas Puzzle” and has major implications for cross-country inequality.

While economists have developed a class of quantitative models to explain bilateral trade flows between countries and predict the effects of a change in trade policy (these are popularly known as “gravity” models) the same modeling has not been applied to international investment positions.

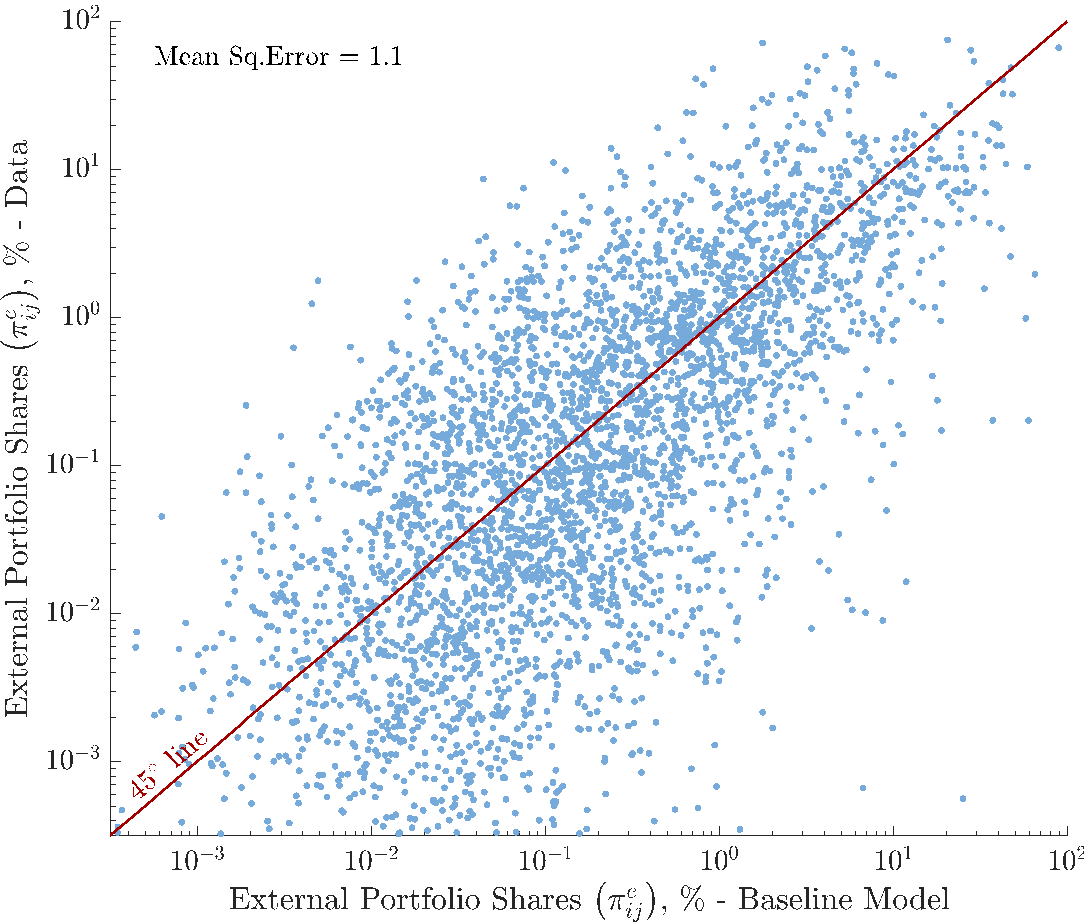

In a recent paper with Enrico Spolaore and Romain Wacziarg (“Barriers to Global Capital Allocation”), we have sought to fill this gap: we produced a first-of-its-kind quantitative model that seeks to account for and simulate production and investment across a wide cross-section of countries. Like trade models, our model can be calibrated with several frictions (i.e. barriers to international investment). These frictions help account for anomalies in international investment data, such as the high degree of home bias that we observe in international investment.

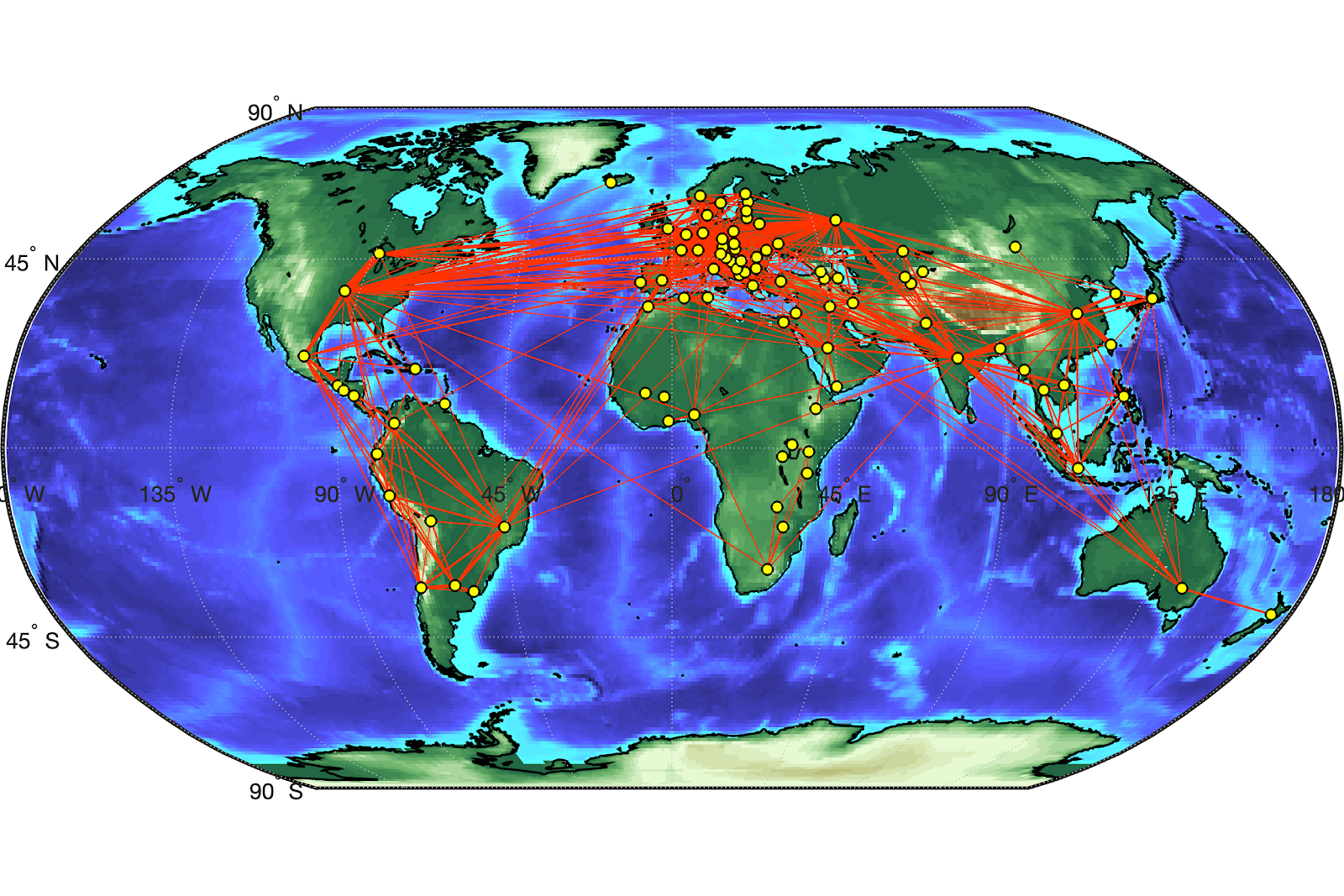

To calibrate the frictions in our model, we have created a novel database of international taxation and geo-political distances between countries, available at geopoliticaldistance.org. This model includes measures of 1) international tax rates on capital (that is, an estimate of the tax rate faced by an investor that wants to invest from country A to country B); and 2) new measures of cultural, geographic and linguistic distance across countries.

We found that these measures of geo-cultural distance across countries play a crucial role in allowing our model to match international investment data. And indeed, our model performs remarkably well in explaining observed patterns of international investment. It accurately predicts bilateral investment positions between countries. It explains why capital is more productive in poorer economies, even when accounting for risk differences. Perhaps most strikingly, it predicts with remarkable accuracy the degree of home bias of the individual countries in our model.

So what is the economic intuition behind these results? The idea is that taxation and geo-cultural differences across countries act as barriers that impede cross-border investment. An investor that wants to invest in a country that is geographically distant, where the tax rate is very high or where the language and the culture are unfamiliar will require a higher rate of return on their investment. As a consequence, countries that are inaccessible (because of geography, culture, language or taxation) end up receiving less capital and produce less income.

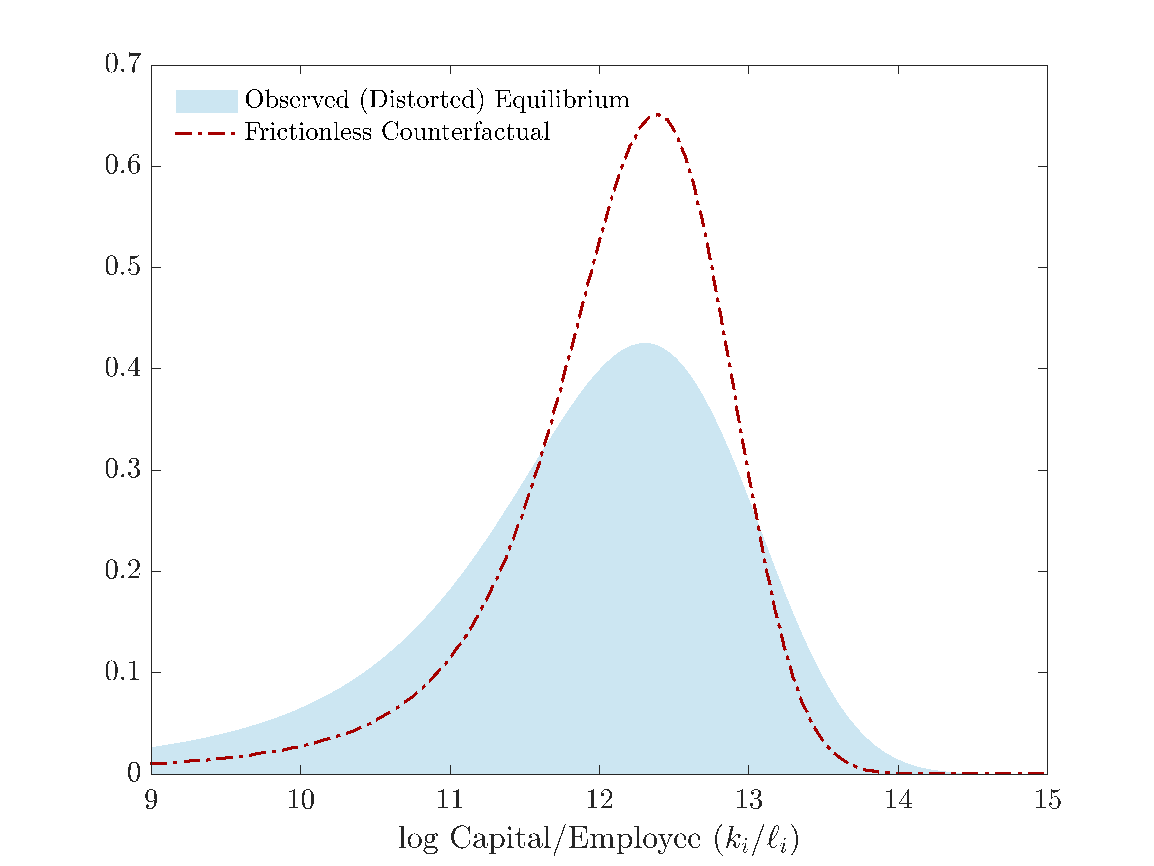

An important purpose of our model is to simulate the effects of removing barriers to international capital flows. The results are striking. We estimate that eliminating these frictions would boost world GDP by nearly 7%—a remarkable efficiency gain. Even more remarkable is the model’s prediction for global inequality: removing barriers would eliminate almost half of the dispersion in capital per employee across countries and a quarter of the dispersion in GDP per capita.

It is well-known that the lack of capital investment is an important determinant of cross-country income difference. Our analysis suggests that the reason why certain countries have struggled to attract investment, despite ongoing globalization, is that they are “isolated” from a fiscal and geopolitical perspective.

In sum, geo-cultural factors appear to be major drivers of the global distribution of capital: they help make sense of many stylized facts about international investment that have long puzzled economists. Moreover, these barriers have enormous consequences for both global economic efficiency and the persistent gaps in wealth between nations. While some of these frictions, like cultural and linguistic differences, may be difficult to change in the short term, others—such as tax policies and regulatory harmonization – offer more immediate avenues for reform.

As the global economy becomes increasingly interconnected, understanding and addressing these barriers to capital allocation will be crucial for fostering inclusive growth and narrowing the economic divides between countries. Our quantitative framework provides a powerful new tool for researchers and policymakers to assess the impact of various frictions and evaluate potential policy interventions in international finance.

Author Disclosure: the author reports no conflicts of interest. You can read our disclosure policy here.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.