New research from Renping Li finds that consolidation among investment banks has produced higher underwriting costs for local governments in issuing muni bonds. Importantly, Li says these costs are not offset by efficiency gains and that the result is a deterioration in local government finances.

This article is part of a series examining the financial conditions of local governments in the United States and the forces that shape them. We will publish a new addition to the series every Monday for the next few weeks.

Security underwriting is a pillar of the financial system, since a bond or equity issuer usually relies on an intermediary to take on the risk of its security before it goes to the open market. Newly issued corporate equity, corporate bonds, and municipal bonds (or “muni” bonds) comprised $102 billion, $883 billion, and $410 billion, respectively, in the United States in 2022. Despite the high volume, some argue that security issuance has not reached its full potential in terms of serving the real economy due to the deterrence of high levels of fees in the underwriting process. In particular, muni bond market watchdogs warned that issuers could “easily be taken advantage of — urged to issue needless or poorly structured bonds, pushed to accept high interest rates or duped into paying hundreds of thousands in unreasonable fees”, which could have put strain on the US K-12 education system.

How should we view underwriting fees? Are underwriters rightfully compensated for performing their tasks, perhaps because security underwriting is inherently intricate and involves considerable risks? What happens when underwriters possess disproportionate market power and earn economic profits beyond the competitive level? In a recent paper, I direct my attention to the muni bond market. Studying consolidating activities as shifters of underwriter market power, I gain insight into its role in shaping the security issuance market.

Local governments usually issue muni bonds to fund infrastructure projects such as roads and water lines. The muni bond market rivals the corporate securities markets in the total volume of issuance nationally. Compared to the corporate securities underwriting market, though, the muni bond underwriting market is much more geographically fragmented. For example, none of the top three underwriters in California during 2010-2020 was a top ten in Massachusetts, nor vice versa. On the contrary, the top ten corporate bond underwriters were the same in these two states with only slight difference in the rankings, and there was also significant overlap in the corporate equity underwriters. Moreover, muni bond underwriting is a dynamic industry which has seen ample consolidation in recent decades. The average HHI based on local underwriter market shares rose from around 1,000 to 1,500 in the past three decades, accompanying 197 mergers and acquisitions (M&As) deals. These features allowed me to study the effects of M&As to understand both the costs and efficiencies that such consolidation produces and, most importantly, its impact on the local governments that rely on the industry.

To do this analysis, I hand-collected data on M&As among all municipal bond underwriters in the U.S. from 1970-2022. I found that 157 M&As occurred among competing underwriters that had geographic overlap and were significant enough to raise the degree of concentration in the local market.

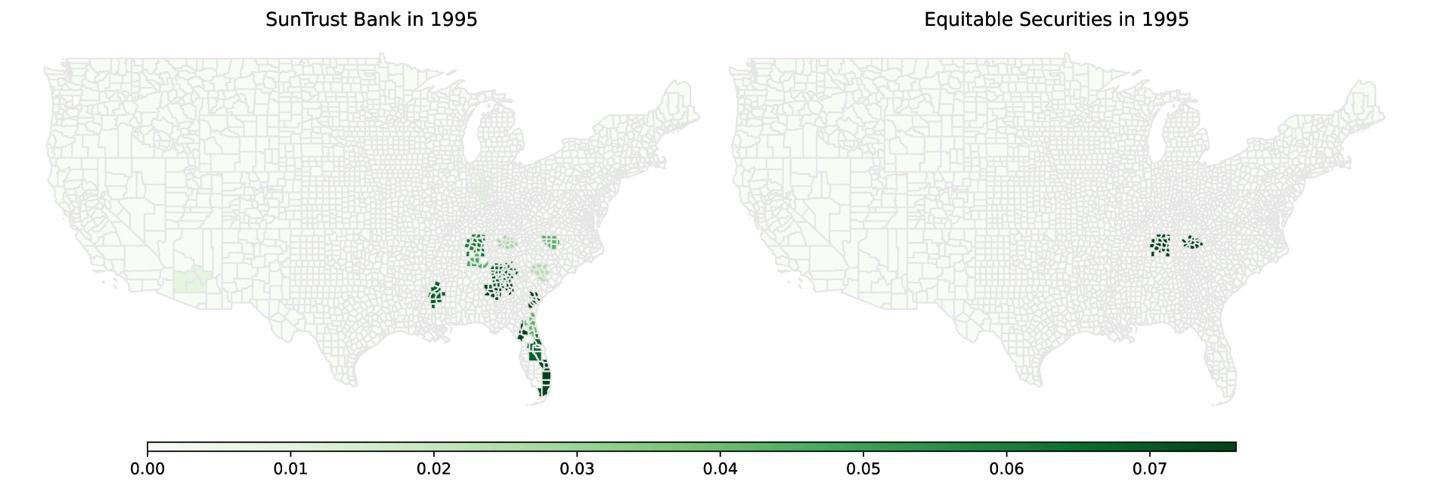

For example, figure 1 shows the merger between SunTrust Bank and Equitable Securities. While SunTrust underwrote muni bonds in many states throughout the Southeast, Equitable Securities was more localized and focused on the state of Tennessee. Their merger would affect the areas where they both operated, such as the Nashville metro area, but not the areas where only one side operated, such as in Florida. For each deal, I look for a control area that is the closest in terms of population and average income but is not affected by consolidation during the same period.

[Insert Figure 1 here, titled “Local Market Shares of Merging Underwriters”]

I first investigated the effects of underwriter M&As on the underwriting spread, i.e., the difference between the offering price to initial investors and the proceeds that the government receives, which is expressed as a fraction of the principal amount and constitutes the revenue of underwriters. I found that the spread rises by 5.7 basis points when there was a merger. For a median bond issue with an amount of $8.4 million, the increase corresponds to a $4,777 greater financial burden on the issuing government. Based on the amount of funding a median county typically raises in a year, this would amount to $19,560 more in the underwriting spread annually.

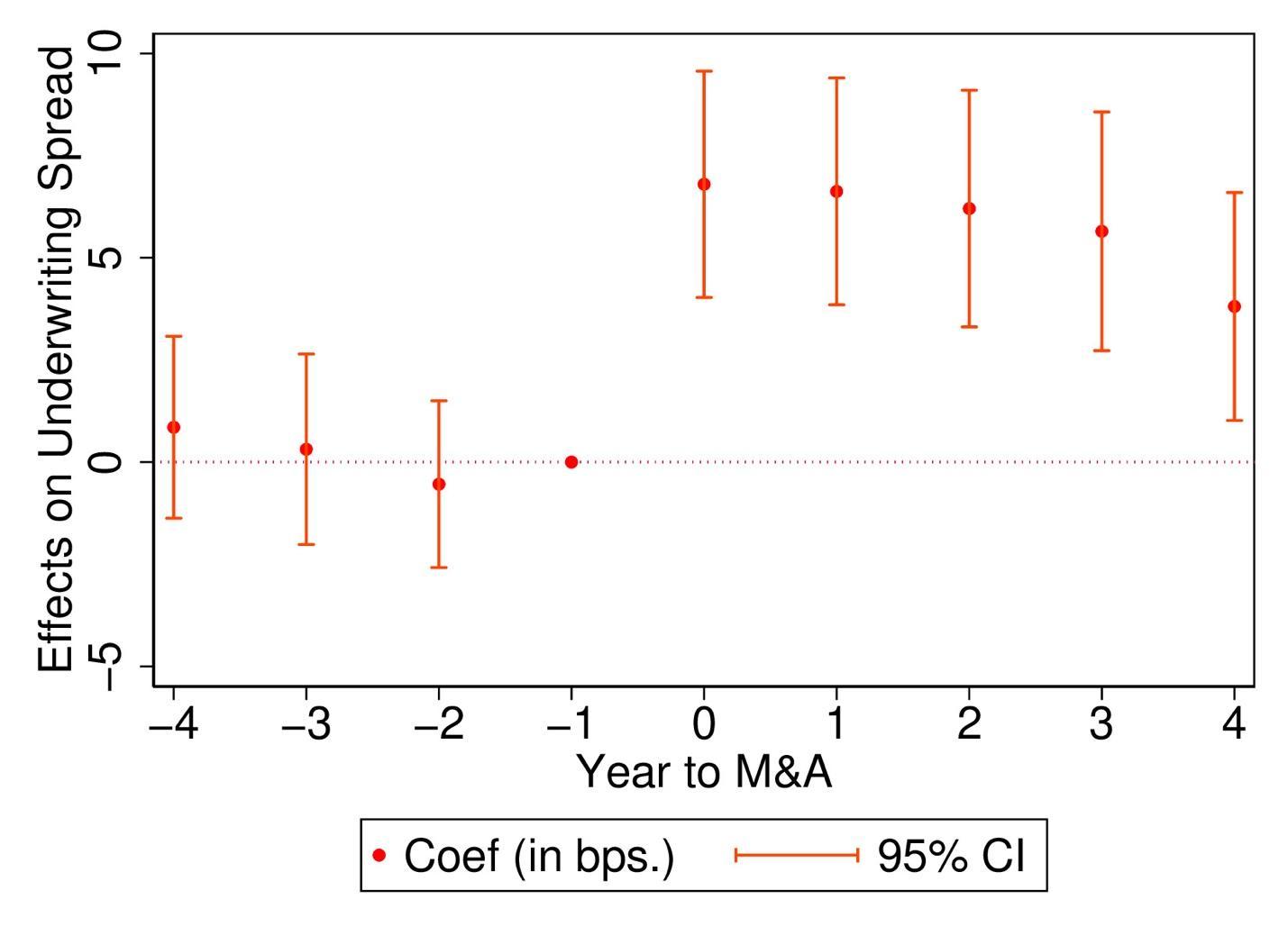

Figure 2 illustrates the dynamics of the difference in the underwriting spread in treatment relative to control areas. The effects doubled for larger M&As that raised the HHI of the local market to a greater extent, tripled in highly concentrated areas with HHI above 2,500, and held in both the early and later parts of the sample period and for bonds of different method of sales, taxable status, or source of repayment. My findings are consistent with price-fixing being the origin of market power and that M&As made new coordination easier to form or existing coordinated interaction more successful or sustainable, which warrants antitrust attention.

[Insert Figure 2 here, titled “Effects of M&As on Underwriting Spread”]

To mitigate the possibility of spurious correlations, I conducted additional tests. The primary concern is that local economic dynamics could be driving both M&A and the underwriting spread. I found that the effects held when I examined scenarios where the M&A-affected areas accounted for only a small fraction of the total businesses of the merging underwriters. In such cases, the M&As were unlikely to be driven by local economic dynamics that could simultaneously affect the underwriting spread. I also classified M&As by their driving reasons according to news reports. The most common reasons are “the acquiror’s desire to gain local/regional dominance”, “desire to expand geographically”, “desire to gain industry-wide dominance”, “synergy from combining different lines of business”, and “synergy from cost management”. While the first two could be related to the local economy, it is unlikely for the rest three. Considering only M&As for which the driving reasons were orthogonal to the local economy, the effects still held. The effects were absent for M&As among underwriters that were geographically apart in their businesses, M&As that were withdrawn, or M&As among purely commercial banks without underwriting services.

The debate on M&A tends to revolve around two major themes: market power and efficiency gains. While I have established that M&A that increases the local market concentration of underwriters lead to a higher underwriting spread, an interesting question is whether issuers were harmed by M&As overall. To answer this question, I next investigated whether there were efficiency gains to the M&A, and, if so, whether issuers enjoyed benefits that could compensate for the rise in the underwriting spread.

What I found was quite interesting: underwriters were less likely to use credit ratings, bond insurance, or financial advisors post-merger, suggesting that there were indeed some efficiency gains to the consolidation. It’s possible that underwriters gained stronger abilities to market and distribute the bonds, making the use of credit ratings or the credit guarantee of bond insurance less necessary. The underwriters might have also acquired expertise that usually resides in the domain of financial advisors, and this kind of in-house integration might have reduced the issuers’ demand for formally hiring a financial advisor. However, I found that the reduction in these costs was way too small to offset the rise in the underwriting spread, and the issuers were, on the whole, negatively impacted by M&A.

Finally, I wanted to validate my findings using data from the Annual Survey of State and Local Government Finances conducted by the U.S. Census Bureau. This data confirmed that the total interest costs borne by local governments nationally increased after underwriter consolidation. The new issuance of debt also dropped in areas that experienced consolidation. A median county impacted by consolidation incurs $0.13 million more in interest payment and cut new issuance by $1.07 million. I also found an overall deterioration in local government finances as their budget deficit ratio, defined as the budget deficit scaled by total expenditures, widened by 1.09 percentage points. These evidence from the survey data is consistent with evidence on the underwriting spread.

President Biden has expressed support for antitrust reform in the banking industry and even signed an executive order directing the Justice Department to work with bank regulators to heighten the scrutiny of bank mergers. The policy debate has also been informed by research showing that bank mergers cause branch closures, raise borrowing costs and fees, reduce credit access, endanger communities’ financial health and safety, and disproportionately impact low- and moderate-income communities. My paper highlights an often-neglected aspect in bank antitrust scrutiny — investment banking activities — that is beyond the traditional scope and yet has significant implications for both the underwriting outcomes and issuers’ overall financial health.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.