The effects of reopening commercial and recreational activities depend not only on legislative provisions but also on the propensity of consumers to return to use these services. A survey of a representative sample of the Italian population shows a widespread propensity to not attend many of the activities in case of reopening, and great caution about returning to pre-pandemic consumption habits.

Many US states are rushing to relax the lockdown measures imposed to help contain the spread of the coronavirus, but new evidence from other countries that went through the same re-opening phase just a few days or weeks earlier is not encouraging.

In Italy, after a gradual re-start of most manufacturing activities, policymakers are considering how to manage the reopening of other “retail” businesses such as bars and restaurants, hair salons, cinemas and theaters, gyms, and swimming pools. These are important sectors of the economy, with strong implications for employment, income, and consumption. In addition to these services, there is also a question on how to return to full public transport capacity, as well as the reopening of schools and religious services. The government has provided a preliminary “roadmap,” but there is much discussion around timelines and processes, as well as regional differences.

Supply Restarts, but What About Demand?

The reopening strategy of the Italian government focuses on the supply side—that is, it aims to restart the economic activities that were suspended due to the pandemic.

However, the effectiveness of this strategy crucially depends on consumer demand. For example, are Italians going back to bars and restaurants once they reopen? Will they use public transportation? Will they visit museums and cinemas? The social isolation measures suppressed demand for many of these activities.

On the one hand, this may have led to a ‘backlog’ of unmet needs, which Italians might feel they want to satisfy as soon as possible. On the other hand, the risk of contagion has certainly not disappeared, and consumers may be inclined to maintain, even in the absence of a strict obligation, some of the measures of physical distancing, for example avoiding visiting public places.

A recent IMF study shows that in the US and the UK mobility and economic activity have fallen considerably even before the introduction of official lockdown measures, and the New York Times reports of a very weak recovery in the States that have already relaxed some of the lockdown measures at the end of April.

Perceptions and Intentions

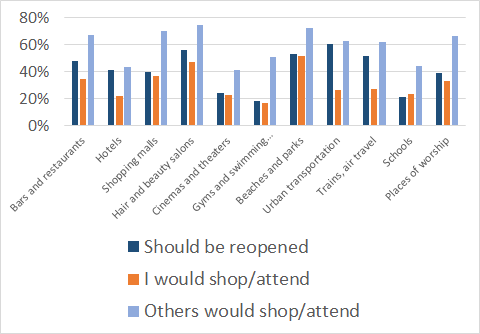

To better understand how demand might have shifted during the pandemic, we conducted a survey between April 30 and May 1, in collaboration with the Italian survey firm SWG, on a representative sample of the Italian population (839 individuals). We asked participants whether they thought that a series of activities should be reopened, their intention to return to shop at or attend places they used to visit prior to the pandemic, and their perception of other people’s willingness to visit those places. Similarly, we asked about their concerns about the reopening of schools if they had children or grandchildren.

Figure 1 shows a sharp difference between one’s own willingness to visit a place, the perception of other people’s willingness to do the same, and the opinions about whether an activity should reopen. In particular, we find that although many interviewees would not be personally inclined to visit most places, they believe that “others” would. This trend is in line with our previous study where we found that a considerable part of the population felt personally able to maintain self-isolation for long periods of time, but few believed that others would be able to do the same. The differences are especially large for the use of public transport as well as for bars, restaurants, and hotels.

With the only exception of schools, the proportion of those who consider reopening appropriate is higher than the proportion of individuals who intend to visit the places. These findings suggest that respondents expressed their judgment about whether an activity should reopen not only on a self-serving basis (i.e., motivated by their own use), but also by considering more general interests, such as the needs of other users (e.g., transport), or the hardship faced by providers of services that were forced to shut down (e.g., bars and restaurants).

Hairdressers Are a “Yes,” Gyms Are a “No“

We also see stark differences in people’s propensity to shop at or visit different places. Although a large share of the sample reports an intention to visit outdoor recreational places such as beaches and parks, as well as hair and beauty salons, only a minority is willing to return to gyms and swimming pools in case of reopening. This can be partly explained by the fear of crowded indoor places, and by the belief held by many that most people would visit these places.

The share of Italians who intend to return to bars and restaurants is also modest. These intentions, if confirmed by actual behavior, warrant caution about a potential recovery in consumption once lockdown measures are relaxed. Furthermore, businesses will have to evaluate whether reopening their activity is economically feasible given the large investments that are required to comply with new safety regulations (e.g. dividers in restaurants, frequent sanitation, etc.).

Despite large territorial variation in the diffusion of the virus, the data does not show major geographical differences. For example, intentions among residents in Lombardy (Milan region), the area of Italy most affected by the pandemic, are very similar to those of residents in other parts of the country.

Still Cautious

Italians seem to be aware of the difficulties and risks associated with reopening, and this might explain their cautious attitude towards returning to normalcy. In fact, only 33 percent of respondents believe that the necessary conditions required to lift the lockdown measures are already in place in their region of residence. 44 percent state that it will take a few more weeks to be ready, and 14 percent a few months; finally, according to 9 percent of the respondents “we are still a long way off.”

Moreover, 40 percent of respondents expect social isolation measures to be reintroduced following a second wave of the epidemic in autumn or winter. 20 percent of the sample predicts that a new lockdown will be necessary a few weeks after the end of the first one, 11 percent expect it in the summer, and 8 percent next year. Only 22 percent think that social isolation measures will never be reintroduced.

One can only hope that Italians’ caution will translate into virtuous behaviors that make the latter scenario more likely.

*A version of this article was published in the Italian website www.lavoce.info.